A Central Bank, as the Federal Reserve currently functions, collectivizes the debit of a nations individuals (US Citizens.)

A debit is something regarded as disadvantageous or unfavorable. For example, the obligation to work for others in the market is a debit that is measured using the standard value metric we call the Federal Reserve Note (or Dollar for short.)

When the boundaries between individuals are eliminated, depersonalization occurs and individual personal traits (such as a person’s debit level) is ignored. Debit is aggregated constituting one “collective” group with debit that is assumed by and shared among all members of the group.

Here is how the Federal Reserve’s website describes collectivized US debit:

The major items on the liability side of the Federal Reserve balance sheet are Federal Reserve notes (U.S. paper currency) and the deposits that thousands of depository institutions, the U.S. Treasury, and others hold in accounts at the Federal Reserve Banks.

If the Federal Reserve had no liabilities then no collectivized US debit would exist and, by extrapolation, nobody in the US would have the obligation (or a contractual agreement) to work. As long as the Federal Reserve has liabilities on it’s balance sheet the US body politic, as a whole, is obliged to share the labor requirement.

To sum it up: people work for Dollars. That is collectivized debit in a nutshell.

So what? …Who works and how much? And what about accountability? It all depends on who has the capital. Whoever has the available money has the capital stock and the preeminence and authority that spending that money affords. The spender is the chief who leads by determining who will work and towards what aim.

There are two ways we traditionally perceive this: (1) the government’s point of view, and (2) commercial banks point of view. The banks take care of the accounting and the government takes care of the leading. Everyone sings kumbyya and the US is the best country in the world.

However, the US is not the only country in the world that is suffering from a currency under continual decay and persistent wealth inequality among members of the collective. This is why we must better understand Government Sponsored Enterprises (GSEs.)

U.S. law allows a number of government-sponsored enterprises (GSEs) to maintain deposit accounts at the Federal Reserve. Like the U.S. Treasury, these GSEs use their accounts to receive and make payments.

The Federal Reserve is the fiscal agent of the U.S. Treasury. Major outlays of the Treasury are paid from the Treasury’s general account at the Federal Reserve.

The Treasury’s receipts and expenditures affect not only the balance the Treasury holds at the Federal Reserve, they also affect the balances in the accounts that depository institutions maintain at the Reserve Banks. When the Treasury makes a payment from its general account, funds flow from that account into the account of a depository institution either for that institution or for one of the institution’s customers.

Reserve Balances with Federal Reserve Banks and Treasury Deposits with Federal Reserve Banks

As a result, all else equal, a decline in the balances held in the Treasury’s general account results in an increase in the deposits of depository institutions. Conversely, funds that flow into the Treasury’s account drain balances from the deposits of depository institutions. These changes do not rely on the nature of the transaction. A tax payment to the Treasury’s account reduces the deposits of depository institutions in the same way that the transfer of funds does when a private citizen purchases Treasury debt. Both actions result in funds flowing from a depository institution’s account into the Treasury’s account.

Reserve Balances as a share of Treasury DepositsTreasury Deposits as a share of Reserve Balances

Now remember that the reason that the Federal Reserve was created was because fractional reserve banking is a legal thing that bank lobbyists support. Namely, “Fractional-reserve banking is the practice whereby a bank accepts deposits, makes loans or investments, but is required to hold reserves equal to only a fraction of its deposit liabilities.” In other words, if a commercial bank can find a credit-worthy borrower who will pay interest on the loan then the bank will profit which is good for it’s shareholders and employees, but the MZM Money Stock will increase.

MZM Money Stock-(Monetary Base; Total/1000):

More than 5,500 depository institutions maintain accounts at the Federal Reserve Banks. They hold balances in those accounts to make and receive payments or to meet reserve requirements.

When the Federal Reserve lends, all else equal, the total amount of deposits of depository institutions increases. When a depository institution borrows directly from the Federal Reserve, the amount the institution borrows is credited to its Federal Reserve account. When the Federal Reserve lends to a borrower that does not have an account at a Reserve Bank, the Federal Reserve credits the funds to the account of the borrower’s bank at the Federal Reserve. When a borrower of either type repays the Federal Reserve, the process is reversed, and total deposits in depository institutions’ accounts at the Reserve Banks decline.

An increase in the Federal Reserve’s holdings of securities also raises the level of deposits of depository institutions. When the Federal Reserve buys securities, either outright or via a repurchase agreement, the Federal Reserve credits the account of the clearing bank used by the primary dealer from whom the security is purchased. Conversely, the Federal Reserve’s sales of securities decrease the level of deposits of depository institutions.

Federal Debt Held by Federal Reserve Banks

During the crisis the US administration determined that the Federal Reserve should have the ability to directly fund government spending, and that that government spending should be put into depository institution accounts at the Federal Reserve.

Federal Debt Held by Federal Reserve Banks/Reserve Balances with Federal Reserve Banks: Since Dodd-Frank

The result is that (1) the Federal Reserve hold much more Federal Debt, and (2) Depository Institutions hold much more deposits on reserve at the Federal Reserve.

So, post Great Recession (1) bank reserve balances at the Federal Reserve stopped tracking treasury deposits and became 1:1 proportional with the Federal Debt that the Federal Reserve holds. (2) bank reserve balances stopped tracking treasury deposits and began tracking long-term Federal Debt owned by the Federal Reserve.

So, what does all of that mean? Well, the Federal Reserve Board of Governors has the ability to regulate depository institutions and enforce capital requirements on them. So, since the Federal Reserve is the fiscal agent of the Treasury, the Treasury has the ability to pass fiscal requirements determined by the legislature on to the depository institutions via the Federal Reserve. Keeping in mind that an important part of depositor institutions income is from the ability to extend loans to credit worthy borrowers within capital constraints that protect against insolvency-caused credit crisis.

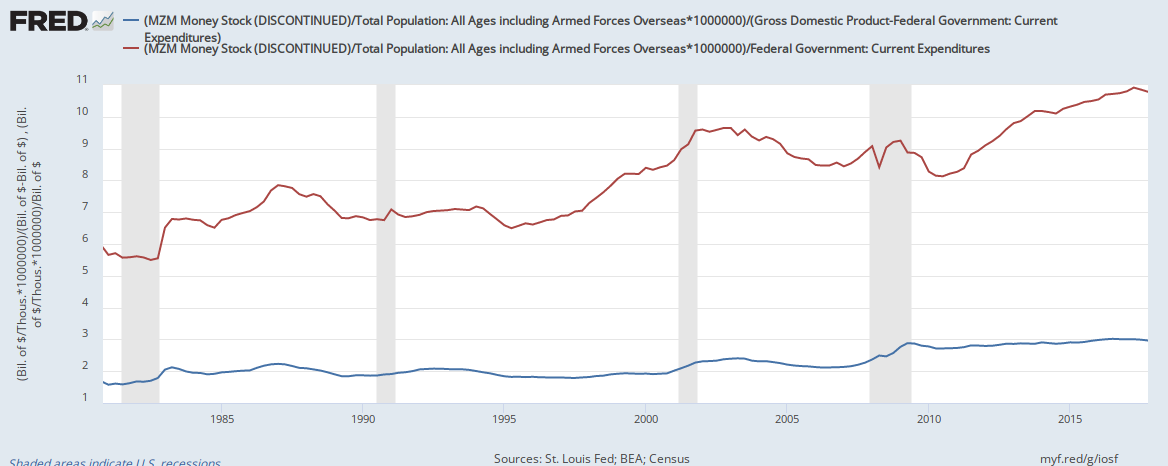

In additional to making sure that the depository institutions are properly accounting, so that the government may lead, the Federal Reserve is mandated to ensure a stable currency and full employment. So, a fiscal standard term is established utilizing the Dollar (the accounting measure,) the population (who all must be dignified with employment,) and government spending (which will allow duly-elected leaders to assign meaningful work for the term):

Term in years of employment contracts (MZM Money Stock/Total Population: All Ages including Armed Forces Overseas*1000000/Federal Government: Current Expenditures)

Now, traditional GSEs lend for housing and traditional banks also lend for housing. They both use capital within constraints to lend. So, essentially they are the same. But, GSEs have accounts at the Federal Reserve that draw from existing collectivized debit, just like the Treasury does. Traditionally, it was banks that grew the stock of collectivized debit outside of sound constraints causing the value of the standard currency to decay, but the Federal Reserve now needs the cooperation from the legislating leader to ensure that banks are utilizing a stable standard while accounting.

Percentage of a Ballot actually spent on average by a member of the collective in a year (GDP/Ballot) and Percentage of a Ballot spent by Forced Government Expenditures on average by a member of the collective in a year (Expenditures/Ballot) [A Ballot is MZM Money Stock/Population]Term of Ballot based on GDP market activity and Federal Government:Current Expenditures [years]But, Government spending is typically a quarter of GDP or less.

Federal Government: Current Expenditures/Gross Domestic Product [Percentage/100]This means that the non-government spending portions of GDP are crowding out the democratically determined decisions of representatives that the Republic’s Ballots put into office to represent us and are essentially represent a significant amount of known trafficking. This reeks havoc on the term (and all market timing):

Term of Ballot: Legal and Illicit components [Years]As can be seen the Term is not fixed as it should be. We could assume that all of the components of GDP that are not federal government current expenditures are not illicit and in fact are governments-sponsored enterprises (GSEs). If we assume that that is the case that states’ budgets, corporate spending, and consumer spending are somehow legitimate then we require policy that allows for the cumulative velocity of the Ballot (MZM Money Stock/Total Population) to fluctuate thus effectively allowing the collectivized term to drift according to market forces.

Market fluctuating collective term of a Ballot (derived from nominal GDP based collective MZM Money Stock Velocity)

When a Depository Institution “prints money” by lending to worthy borrowers and raising the M2 money stock it is effectively stealing some spending ability from Congresses’ Appropriations budget for the fiscal year. Remember, the Federal Reserve, and by extension depository institutions, are fiscal agents of the Treasury. Congress has budget caps which limits current fiscal year expenditures proportionally to Ballots (constituents which representatives are spending on behalf of.) So, this is a contributing factor that seems to give Congress feeling to raise the budget caps. The rational thing is to determine policy that pre-specifies what share of the Fiscal Year Budget each GSE is responsible for. Fiduciaries with accounts at the Federal Reserve are GSEs and are therefore legitimized to appropriate a share of the Federal Government: Current Expenditures each Fiscal Year. It is Congresses purview to agree upon the appropriation of percentage shares of Federal Government: Current Expenditures each Fiscal Year among fiduciaries. Then, it is the fiduciaries’ preview to determine how shares of each fiduciaries’ shares are to be spent on subsidizing agencies. There are a total of 535 members of congress who are fiduciaries. Depository Institutions are fiduciaries. The Federal Reserve is a fiduciary. The President is a fiduciary? In a positive sense in that it is the fiduciary of funded agencies. In a negative sense due to veto rights. Are the Judicial Branch a Fiduciary? Only in a negative sense. Fund flows determine hierarchy power structure.

We can judge the effective inflation rate required to make up for lack of adequate income tax receipts and compare that to the effective federal funds rate (overnight inflation rate) levied by the Federal Reserve:

Share of Federal Government Current Expenditures not covered by income taxation in a Fiscal Year as percentage share of Ballot (red). Effective Federal Funds Rate (blue) [percentage][Take Away 1: lowering the Federal Funds Rate may cause recessions (due the the Federal Reserve selling Treasury Debt.]

The difference between the required overnight annual inflation rate (based on actual Federal Expenditures and Tax Receipts) and the overnight annual inflation rate actually levied by the Federal Reserve. {red line minus blue line above} [percentage]

[Take Away 2: Ease money (the line above 0.0, more spending than taxes) may cause productivity growth (or less inequality,) rather than inflation. Tight money (the below above 0.0, more taxes than spending) may cause recessions (due the the Banks selling Treasury Debt.)]

So, it appears that leading up to the Great Recession the Federal Reserve was levying an overnight inflation tax (paid by banks) sufficient to make up for insufficient income tax receipts to fund actual government expenditures. The budget was essentially balanced when the line traced 0.0.

Bank Lending is government borrowing via the reserve requirement. This is why bank lending counts towards Federal Government Current Expenditures. Also, this is a considerable reason why banks should solely bear the inflation tax for the collective as the federal funds rate rather than income and capital gains taxing everyone.

Desired overnight annualized inflation tax rate as derived from government expenditures (red), Actual as derived from federal funds rate (blue)

To achieve that the legislature would cap spending/expenditures at a fixed rate that does not change from year to year. Then, the Federal Funds rate would rise to that same rate. So, the blue line would be on the red line above and the line would be flat at the rate chosen for Congress to keep from now on. Then deposit institutions would pass that inflation tax on to depositors since the legislator will likely take over the fiduciary ability that banks have to lend government expenditures at a profit and elect to spend that money on their constituents directly as their constituents see is best instead. This eliminated the risk depository institutions pose in causing another recession, or business cycle downswing, while raising funds that pay for government expenditures with an explicit tax on each Dollar in a persons possession which is collected by depository institutions and returned to the Treasury via the Federal Reserve. The result is a surplus that is equivalent to tax receipts from the existing IRS tax code. Therefore, the income tax and capital gains taxes can be entirely eliminated and the financial security the the existing 20 trillion in debt provided to Treasury investors (such as retirees) is maintained.

")

")

The difference between the required overnight annual inflation rate (based on actual Federal Expenditures and Tax Receipts) and the overnight annual inflation rate actually levied by the Federal Reserve. {red line minus blue line above} [percentage]

The difference between the required overnight annual inflation rate (based on actual Federal Expenditures and Tax Receipts) and the overnight annual inflation rate actually levied by the Federal Reserve. {red line minus blue line above} [percentage]